Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Tight retail market leaves fewer options in new buildings

Favorable demographic trends, strong demand and a lack of speculative construction have led to Atlanta’s tightest retail market on record, with the majority of available space now resigned to aging, outdated properties.

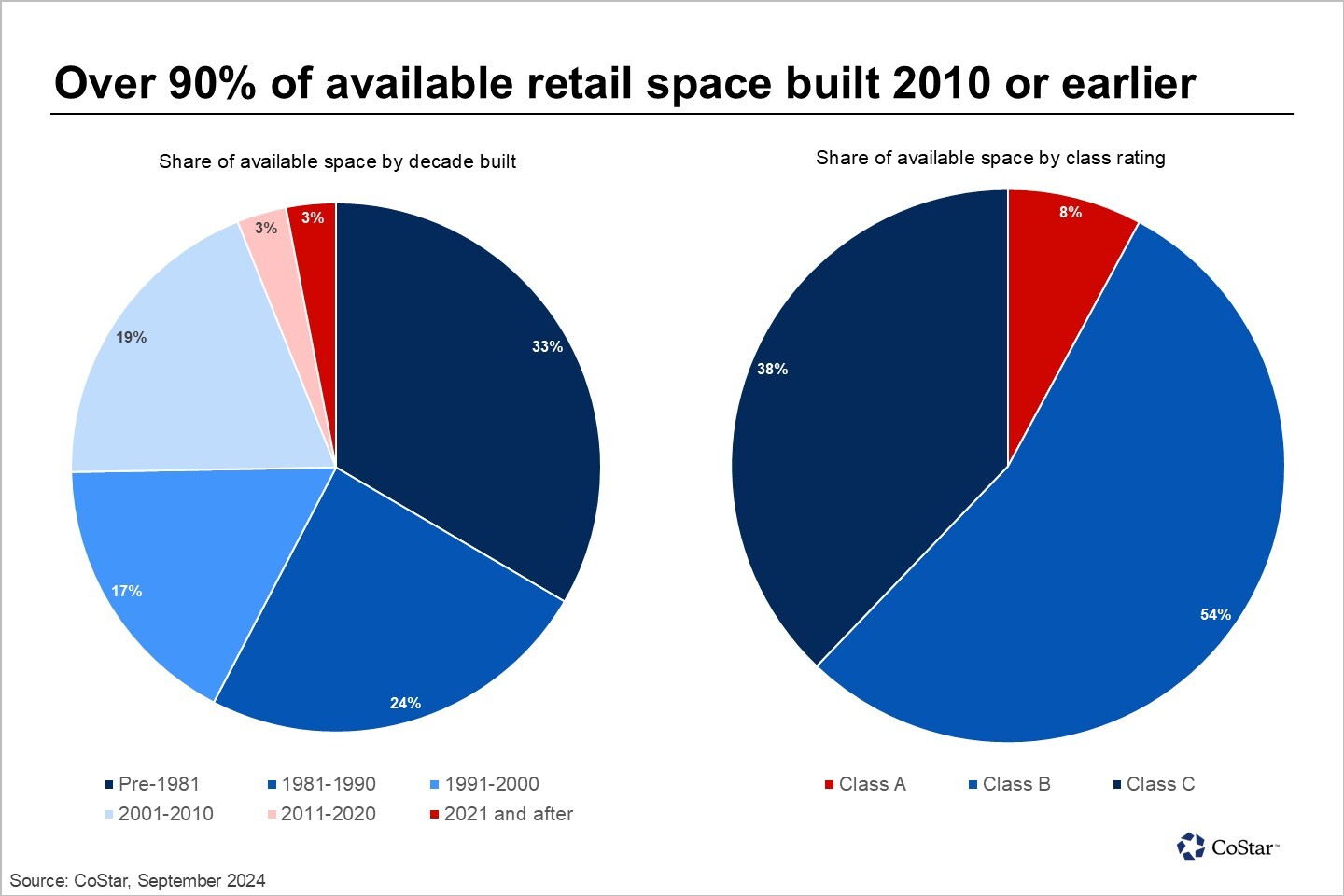

While the region’s 3.7% availability rate is about 210 basis points lower than the area’s 2014 to 2019 annual average, more than 50% of all available retail space in the market is considered Class C, according to CoStar data. Class C properties are typically older, in fair to poor condition and not as well-located as a Class A or Class B building.

Additionally, 33% of all available space was built before 1981.

Higher-quality space in new buildings is the most difficult to find. Roughly 91% of available retail space in Atlanta was built before 2011, and only 8% of available space is considered Class A.

The lack of new construction has led to an increasingly difficult market for tenants seeking well-located space in high-quality properties. The total inventory has grown by less than 5% over the past decade, CoStar data shows, while the population has increased by about 15%.

The availability rate for space in properties built since 2011 is just 2.8%, about 90 basis points lower than the area average. For the higher-quality Class A buildings, just 2.4% of space is available. This lack of new and high-quality space mirrors national retail trends.

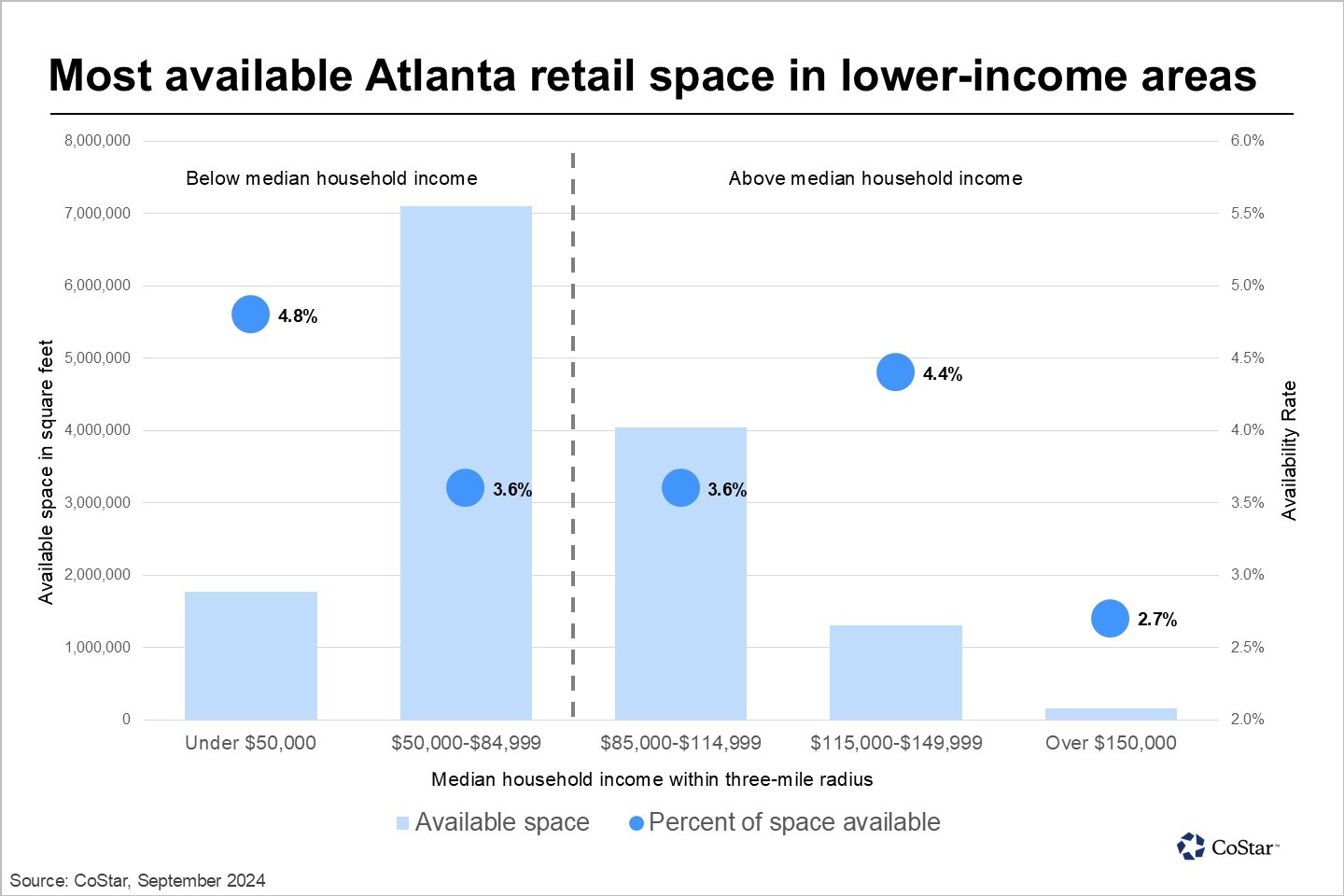

Retailers often flock to areas with significant population density and greater buying power. However, over 60% of retail space is located in areas with a median household income below the market average of about $87,000. That includes Norcross, Stone Mountain and Covington.

Some retailers, such as dollar stores or discount supermarkets, perform well in lower-income areas. However, segments with higher-cost products and services need to target higher-income neighborhoods. Only about 1.5 million square feet of retail space is available within 3 miles of areas with a median household income of over $115,000, such as Johns Creek, East Cobb and Alpharetta.

Elevated interest rates have further muted retail construction in Atlanta. The construction pipeline in the second quarter was about 55% smaller than in 2023, CoSta data shows. About 730,000 square feet of retail is currently being developed.

Roughly 75% of the new space is preleased by tenants, including a car dealership, gas stations, Publix, Starbucks and Chipotle. With only about 200,000 square feet of available space under construction, tenants seeking new buildings will be in a competitive market. Elevated construction costs also mean retailers are more likely to stay put as building our space has become less accessible.